| …But does that mean that oil prices will only go down from here? In this new interview with Elliott Wave International’s Chief Energy Analyst, Steve Craig, you’ll learn where he sees prices going next. *Editor’s note: this interview was recorded on August 12; the price low cited in the video was broken on August 13. READ MORE |

EURUSD – What is Next?

| Think the recent rally in the euro was the result of “good news” from Greece? Think again. Watch our Currency Pro Service editor, Jim Martens, explain what’s really behind the moves. “Trading Forex: How the Elliott Wave Principle Can Boost Your Forex Success” In this free 14-page eBook, our Senior Currency Strategist Jim Martens pulls READ MORE |

Greek Tragedy? Too Late to Prepare

| Today, I got on the phone with Brian Whitmer, editor of our monthly European Financial Forecast. Brian has been preparing his subscribers for the Greek crisis for a while. Listen to his latest thoughts. Europe is in the world spotlight this month, with Greece’s future hanging in the balance. But Greece is just one part READ MORE |

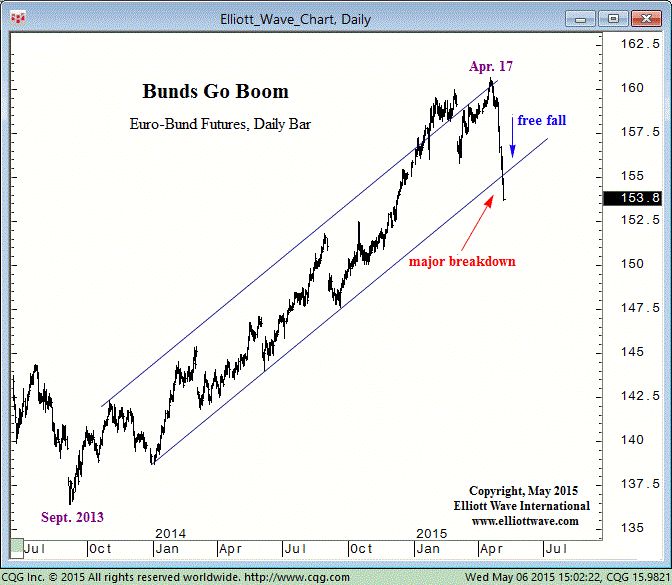

Volatility Shakes Bond Markets

| Is the debt bomb about to go off? The yields on U.S. Treasuries and European sovereign debt have risen sharply in a relative short time. Bond prices trend inversely to yields — which means debt portfolios have suffered substantial losses. From mid-April through May 6, yield on German 10-year bunds spiked 47 basis points. Yields READ MORE |

NASDAQ Leads the Stock Market Bubble

| Another bubble is about to pop. In March 2015, we covered the return to a popular fascination with technology. The striking resemblance to 2000’s technology mania is not going unnoticed. How can it? With the NASDAQ’s much heralded return to 5000 and magazine covers proclaiming “Google Wants You To Live Forever,” concern about an “asset READ MORE |

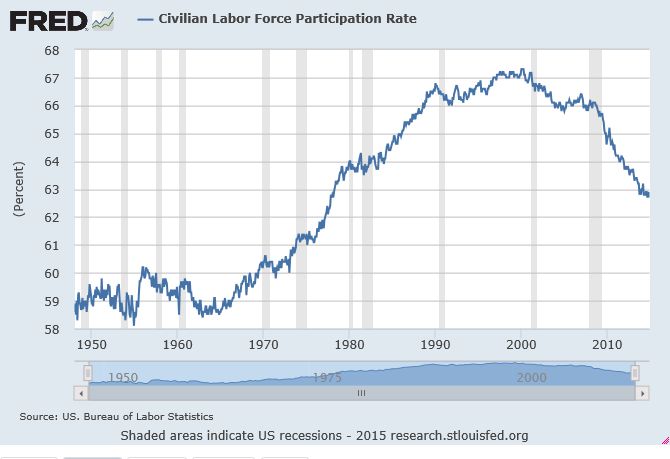

Is Unemployment Rate Really Getting Better?

| The “Big Lie” About the U.S. Jobs Picture Some 30 million people are either out of work or severely underemployed Get Your FREE Special Report: What You Need to Know NOW About Protecting Yourself from Deflation » The financial media heve been featuring stories with an upbeat outlook for the U.S. economy. For example: The READ MORE |

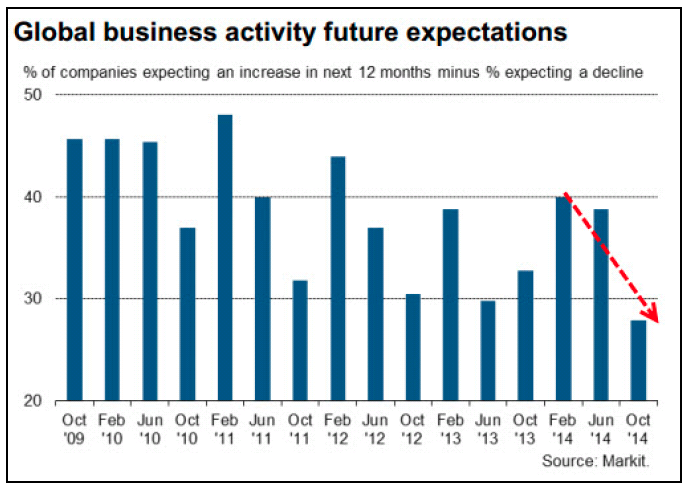

Why Expectations for Business Activity are Plunging

| Editor’s note: This article is excerpted from “The State of the Global Markets 2015 Edition,” a comprehensive report by Elliott Wave International, the world’s largest independent market-forecasting firm (data through December 2014). You can download the full, 53-page report here — 100% free. In its November issue, published on Oct. 31, EWI’s European Financial Forecast READ MORE |

3 Ways To Identify Support and Resistence

| We will consider three ways to identify price support and resistance in the markets you trade. Previous highs and lows Trendline support Fibonacci Ratios These examples are adapted from Jeffrey Kennedy’s time tested Trader’s Classroom service. 1) Uptrends terminate at resistance while downtrends terminate at support. Previous highs and lows often act as resistance and support. In READ MORE |

From Faith to Failure: Abenomics

| After decades of deflation in Japan, we thought there was hope and the deflating money supply and falling prices were gone. But during the last two quarters we once again witnessed relentless deflationary pressure in Japan despite record stimulus that promised inflation. Well, inflation is missing in action. Deflation still rocks the nation! Surprised? Why READ MORE |

Can Europe’s Deflation Be Like Japan?

| While the stock market has recently seen all time highs in the the United States, despite Federal Reserve’s quantitative easing runs, inflation has been mute. In fact there is talk that FED may just keep printing money if deflation continues to be a concern! Across the ocean, money printing has continued for some years as READ MORE |

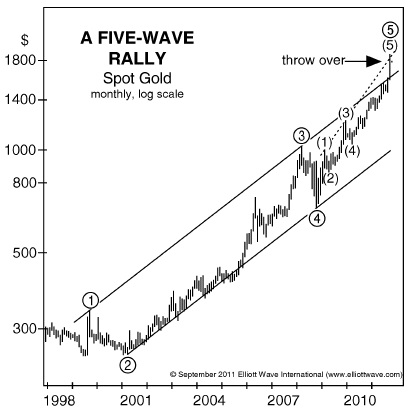

Gold Price Direction

| Where is the gold price heading? Will gold keep crashing? Since hitting a record high of $1921.50 per ounce in September 2011, gold prices have erased 30% in value. By the end of day on October 3, 2014, gold prices were circling the drain of a 15-month low. After such devastation, the global community of READ MORE |

Prepare for the Stock Market Crash

| How to Prepare for the Coming Crash and Preserve Your Wealth Bob Prechter first released Conquer the Crash: You Can Survive and Prosper in a Deflationary Depression during a stock-market high in 2002, and it quickly became a New York Times–bestseller. Now he has updated the book with 188 new pages for a second edition, READ MORE |

How to be safe in an economic crash

| People worry. Sometimes it helps, sometimes there is nothing we can do. I came across some research on the subject of worry. Here’s how it was presented: Things People Worry About: things that never happen – 40% things which did happen that worrying can’t undo – 30% needless health worries – 12% petty, miscellaneous worries READ MORE |

Why Do Traders Fail?

| The following is an excerpt from Jeffrey Kennedy’s Trader’s Classroom Collection. Now through February 6, Elliott Wave International is offering a special 45-page Best Of Traders Classroom eBook, free. I think that, as a general rule, traders fail 95% of the time, regardless of age, race, gender or nationality. The task at hand could be READ MORE |

Jaguar Inflation

| FED rate is at 0% and some people are worried about inflation that may come as the recovery takes hold. Some other people believe deflation is the problem and FED rate should stay at 0%. So, is it really the FED who sets the interest rates in an economy? Utimately, FED does not control the READ MORE |