| Sometimes you know that a company earnings will be good. You buy the stock and you wait for the earnings announcement. Stock goes up until the good news are out. And then it sells off and you are frustrated. Sometimes you see the market crashing in the morning, the media says “home builders are in READ MORE |

DOW Jones Index Priced in Gold

| DOW Priced in Gold: What Does It Mean for the Long-Term Trend? Of the many forward-looking market indicators we at EWI employ, one of the most interesting tools (and least discussed in the financial media) is the DJIA priced in gold — “the real money,” as EWI’s president Robert Prechter calls it. What implications might READ MORE |

What Can Movies Tell About the Stock Market

| What Can Movies Tell You About the Stock Market? The following article is adapted from a special report on “Popular Culture and the Stock Market” published by Robert Prechter, founder and CEO of the technical analysis and research firm Elliott Wave International. Although originally published in 1985, “Popular Culture and the Stock Market” is so READ MORE |

Extreme Sentiments Threaten European Union

| The similarities between Greece and pre-WWII Germany are striking Extreme sentiments threaten Europe. Nazi salutes. Praise for Adolf Hitler. Swastika-like banners. Now, before you write off this warning as a run-of-the-mill, Nazi-name-dropping scare tactic, consider this recent report from the Socionomics Institute, a U.S.-based think tank that studies global trends in social mood. Here’s an READ MORE |

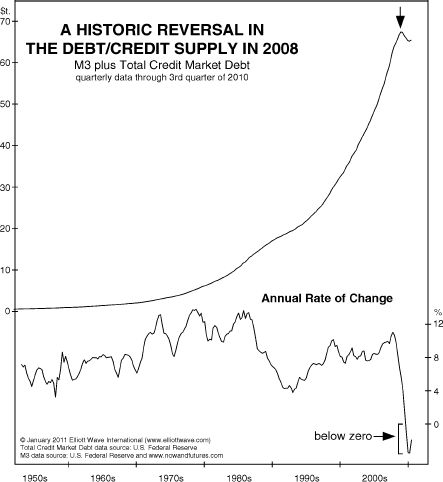

Deflation in Europe

| History shows that the U.S. should pay attention to economies in Europe The economy has been sluggish for five years. There’s no shortage of chatter about “why,” yet few observers mention deflation. One exception is a hedge fund manager who spoke up at the recent Milken Institute Global Conference. The presentation by Dan Arbess, a READ MORE |

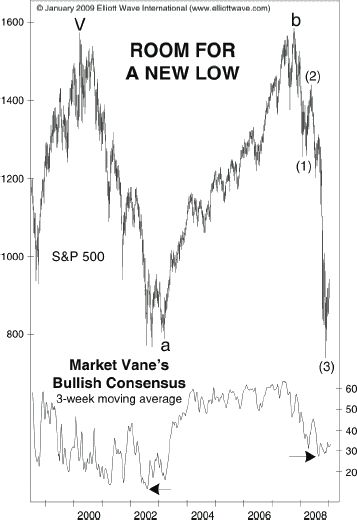

Extreme Sentiment Signal Stock Market Top

| EXTREME SENTIMENT SIGNALS TREND CHANGE In March 2009, stock prices were at a 12-year low, and the Dow Industrials were down 54% from the 2007 peak. You’d have needed to search far and wide to find someone calling for a rebound. Most investors feared that more of the same was ahead for stocks. But on READ MORE |

How Deep Will the Cuts in Government Services Go?

| “Localities have chopped 535,000 positions since September 2008…” USA Today (10/18) Cuts in government services became conspicuous after the 2007-2009 financial crisis. The first edition of Robert Prechter’s Conquer the Crash saw this coming, even though the book published nearly a decade ago: “Don’t expect government services to remain at their current levels…The tax receipts READ MORE |

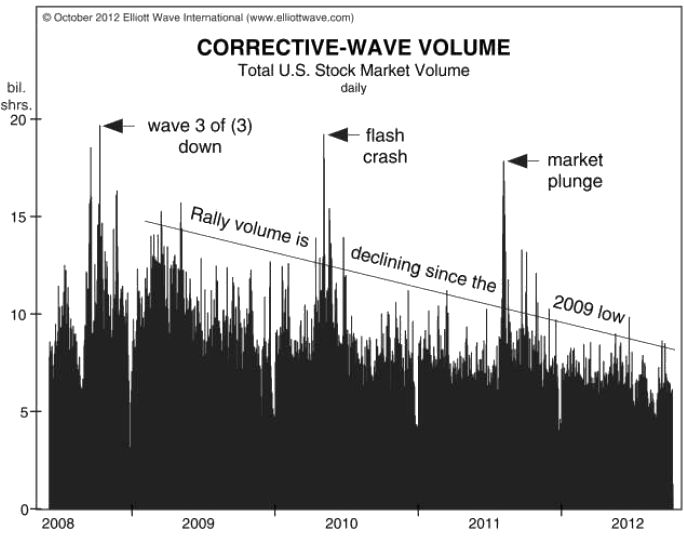

Declining Volume Spells Trouble

| Declining Volume Signals Market Trouble The three-and-a-half-year rally has occurred on declining volume What a comeback for the Dow Industrials! From a March 9, 2009, close of 6,547, the senior index climbed to 13,610 on Oct. 5, 2012. Moreover, the Dow achieved this feat in the face of a weak-kneed economy, and it has grinded READ MORE |

Stock Market Crash – How Low Can it Go?

| The stock market had ups and downs but over all we did fairly well. Unemployment remains stubbornly high but bonds and equities and recently housing had price gains. At least that has been the story of the last two years even though Asia and European markets have topped and have been declining since 2010 and READ MORE |

Is Your Bank Safe?

| Bank failures continue to increase every year since the recession begun. FDIC guarantee is still 250,000 dollars. But if dominos start falling, will FDIC be able to guarantee your bank accounts? Or should you consider looking into the safety of your own bank? World’s 15 Biggest Banks Get Downgraded Another one of Robert Prechter’s Conquer READ MORE |

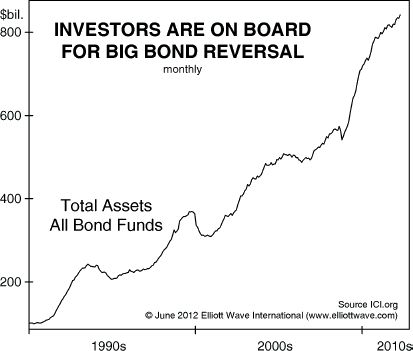

The Bond Market Bubble is About to Pop

| Why risk in the rebalanced portfolio is getting bigger Surprisingly, after the great stock market run of 1980s and 1990s, a decade of ups and downs in stocks left bonds ahead. Yes, bonds have outperformed stocks for the last 30 years. But how long can the bond miracle last? Bonds are deemed to be stable READ MORE |

How Does Money Disappear?

| In 2008, after a day of major crash George Bush went on TV and said a trillion dollars of wealth has just disappeared. Is that really true? Is it really the case that people had a combined trillion dollars that just evaporated when the market crashed? How Does Money Disappear? The bursting of the “debt READ MORE |

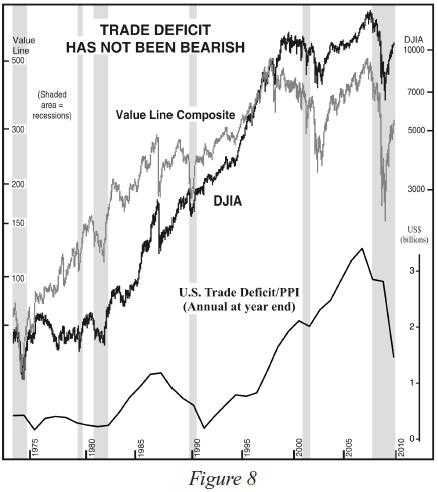

Is Lower Trade Deficit Bullish for the Market

| US trade deficit is lower for the past year and the government is trying hard to further lower it. Deficit cannot be maintained forever so we have to do something about it and the government is motivated. It makes sense to have a balanced trade for the overall economy. But is that something to celebrate READ MORE |

Does Deflation Remain a Threat?

| A 90-Page “Deflation Survival Guide” Gives the Answer “Every excess causes a defect; every defect an excess. Every sweet hath its sour…The waves of the sea do not more speedily seek a level from their loftiest tossing, than the varieties of condition tend to equalize themselves.” This quote comes from Ralph Waldo Emerson’s essay, “Compensation.” READ MORE |

Money, Credit and the Federal Reserve Bank

| Money, Credit and the Federal Reserve Bank The world’s foremost Elliott wave expert Robert Prechter goes “behind the scenes” on the Federal Reserve The ongoing economic problems have made the central bank’s decisions — interest rates, quantitative easing, monetary stimulus, etc. — a permanent fixture on six-o’clock news. Yet many of us don’t truly understand READ MORE |